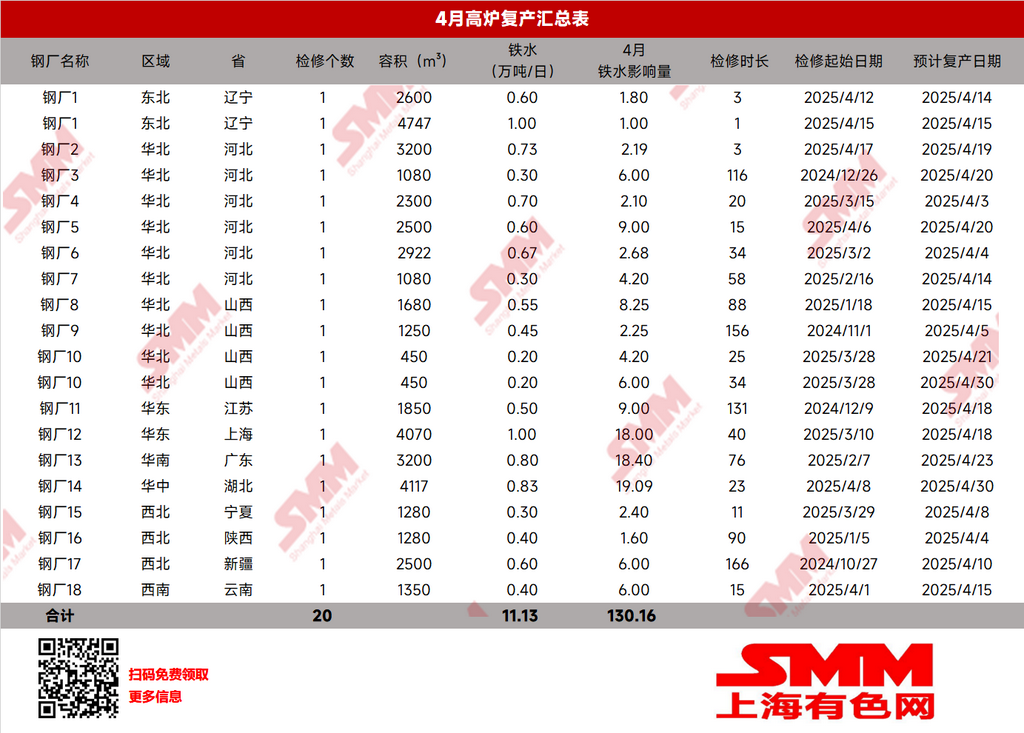

According to SMM's tracking and survey data, in April, there were actually 7 new blast furnaces undergoing maintenance, resulting in a daily reduction of 46,600 mt of pig iron production. The concentrated maintenance of blast furnaces was mainly in north China. Meanwhile, 20 blast furnaces resumed production, leading to a daily increase of 111,300 mt in pig iron production. Among them, Hebei and Shanxi provinces had the most concentrated number of blast furnaces resuming production. SMM survey data showed that in April, the maintenance of blast furnaces led to a net reduction of 4.5956 million mt in pig iron production, a decrease of 1.9387 million mt MoM from March. The daily average pig iron production at month-end in April increased by 41,500 mt MoM from the end of March

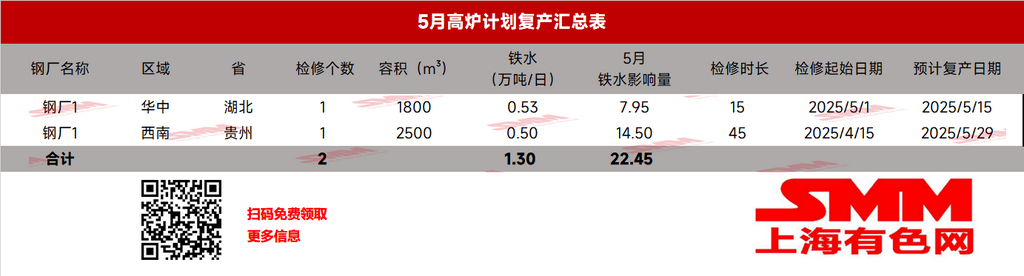

. According to SMM's tracking and survey, as of now, in May, there are plans for 6 new blast furnaces to undergo maintenance, which will reduce daily pig iron production by 37,300 mt; in contrast, there are plans for 2 blast furnaces to resume production, increasing daily pig iron production by 13,000 mt. Based on existing data statistics, it is expected that in May, the maintenance of blast furnaces will affect a total of 4.0873 million mt of pig iron production; a decrease of 500,000 mt from April. Pig iron production in May is expected to drop back slightly. According to SMM's estimate of daily average pig iron production, on May 28, the daily average pig iron production of the sampled steel mills is expected to be approximately 2.4327 million mt, a decrease of 20,800 mt MoM from the end of April

. Entering May, the off-season effect of end-use demand has gradually emerged. Although steel mill profits are currently moderate, end-use demand is gradually weakening; coupled with the fact that steel mills in some provinces have already received requirements to reduce crude steel production. Therefore, SMM expects that the actual number of blast furnaces undergoing maintenance in May will be higher than currently reported. SMM will continue to track the relevant situation on a weekly basis

.

![Before the holiday, the black chain is unlikely to see a trend-driven market [SMM Steel Industry Chain Weekly Report].](https://imgqn.smm.cn/usercenter/zUFfM20251217171748.jpg)

![[SMM Chromium Daily Review] Inquiries and Transactions Weakened, Chromium Market Showed Mediocre Performance Before the Holiday](https://imgqn.smm.cn/usercenter/ENDOs20251217171718.jpg)